- Markets

- Cap & Trade

- Clean Fuels Standard

- Carbon Offsets

- Carbon Linked Mechanisms

- Get to Know

- Market Coverage

- Cap & Trade

- Clean Fuels Standard

- Carbon Offsets

- Carbon Linked Mechanisms

- Use Cases

- About us

- Membership Plans

- CAFÉ

- Cap-and-Trade

- Clean Fuel Standards

- Carbon Offsets

- Price Commentary

- Weekly Commentary: ICE CCA weekly volumes drop to 18.5M tons as new front receives weak participation

Weekly Commentary: ICE CCA weekly volumes drop to 18.5M tons as new front receives weak participationWCI CaT Monday, 2nd August 2021

Monday, 2nd August 2021 Craig Rocha

Craig RochaSummary:

- ICE CCA weekly volume fell to 18.5M tons, down by 58%

- Front rolled over from Jul21 to Aug21, 16.9M tons of OI closed(CFTC)

- Fund managers remain bullish, increase net long positions by 1.6M tons

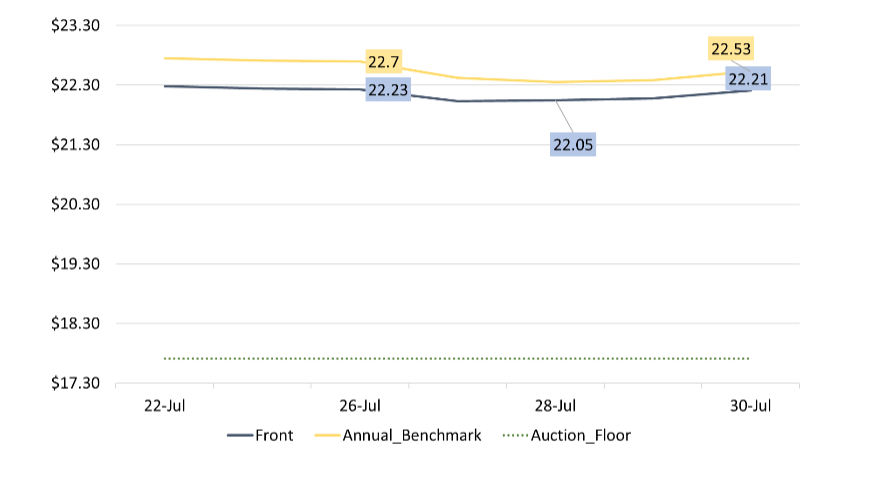

Last week at the InterContinental Exchange, CCA volumes dropped to 18.5M tons while the front rolled over from Jul21 to Aug21 on Wednesday. The secondary market front closed at $0.03 lower as uptake for the new front was poor.

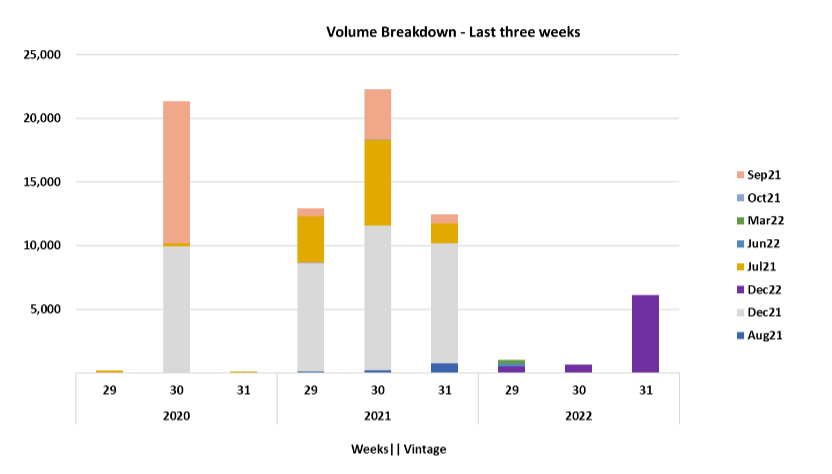

16.9M tons of V21 Jul21 contracts expired; only 0.5M tons of fresh OI appeared on the Aug21 contract. Additionally, the post-auction contract V21 Sep21 saw 0.6M tons of new OI. The benchmark contracts saw net closures of 2.2M tons.

Market participants were expecting upward movement around the front rollover. Day wise volumes were highest on Tuesday and Wednesday when the front rolled over to Aug21. And trading volumes on the Dec21 and Dec22 contracts were over 60% of each of those days’ total volume. On the day of front expiry, 2.9M tons of OI on Dec21 was registered. However, the Dec21 contract lost $0.04 after poor OI creation on the new front and 3.5M tons of Dec21 were closed on the following day.

The secondary market front last traded at $22.19 which is $4.48 above the auction reserve price, making it a good time to purchase the post-auction contract Sep21. However, Sep21 only received 0.6M tons of new OI last week. At present, there are 12.7M tons of positions on the V21 Sep21 contract and 11.9M tons on the V20 Sep21. The V20 Sep21 contract was purchased specifically for compliance; V20 allowances may only be used for Compliance Period three (or later) obligations. Although, the V20 Sep21 positions have reduced by half since April 2021, owing to the steep rise in CCA prices in between and also due to updated facility emissions last reported to CARB in June. Overall participation was weaker than expected and if spills over to the next week, the front could see downward price movement.

The latest CFTC data (27th July) presents that compliance entities reduced net long positions by 1.2M tons while fund managers increased net long positions by 1.6M tons. Swap dealers did not report any noticeable change.

The upcoming auction is expected to supply an additional 14M allowances from last year’s undersubscribed auctions. The $4.48 gap between the auction floor and the secondary market makes a good case for arbitrage. But, CCA prices have seen downward corrections in the last few weeks and some speculators may wait and watch this week. Compliance demand on the secondary market would also remain low while speculator participation could shoot up mainly around price movements.

*WoW Change reported between 22nd July and 29th July.

Analyst Contact:

Anant Jain (anant.jain@californiacarbon.info)

You might also like Article

Article

Interviews

Interviews

News

News

- Clean Fuel Standards

- Clean Fuels Standard

- Cap & Trade

- Clean Fuels Standard

- Cap & Trade